If you spent any amount of time listening to the nattering voices of the negative, chances are you've heard any number of rumors, lies and half-truths about the Patient Protection and Affordable Care Act, aka Obamacare or ACA. Allow us to help you sort it out.

Why is Health Care an Issue?

The U.S. spends more money per capita for health care than any other nation, yet we rank 37th in terms of outcomes: Life expectancy, and infant and maternal mortality are among the worst of all developed countries. Rates of obesity, heart disease and diabetes are epidemic.

In Mississippi, about a half-million people live without any health insurance, leaving them at risk for more severe, advanced-stage illnesses and catastrophic medical costs when the unexpected happens.

When large percentages of the population are unable to get basic, preventive medical care, it puts the economy and well being of the nation at risk. First, it's much cheaper to pay for preventive care than emergency care. Second, healthy citizens mean a more productive work force.

How Does Obamacare Help?

The Affordable Care Act attempts to establish minimum standards of health care for the majority of U.S. citizens, making preventive care--flu shots and pap smears, for example--available without deductibles, co-pays or co-insurance. It also reins in some of the harshest practices of the health-insurance industry. Under the law:

• Insurance companies cannot deny coverage due to pre-existing conditions.

• They cannot charge higher rates to women and must eliminate annual and lifetime limits for coverage (where companies set a maximum dollar amount of coverage).

• Insurance companies can no longer cancel a policy because you get sick or make a mistake on an application.

• Parents can keep their children on their policies until they hit age 26.

• Many older Americans will see a substantial reduction in premiums as a result of changes.

• Insurers will be held to higher administrative standards. They must spend 80 percent of your premiums on health care, and proposed rate hikes of more than 10 percent are subject to new scrutiny.

True or False?

With so many rumors out there, you'd think Obamacare was a mythical unicorn (or Bigfoot) instead of a law written on paper. Here are just a few of the myths spread about the law. Test yourself, then see the answers, below.

- (R) True (R) False Obamacare is a socialist takeover of medicine.

- (R) True (R) False Government bureaucrats will be able to cut off treatment to grandma.

- (R) True (R) False Unions are exempt.

- (R) True (R) False Taxpayers will pay for abortions.

- (R) True (R) False Obamacare will kill jobs.

- (R) True (R) False Health care is best left to the free market without government interference.

- False. Under socialism, the government (or a collective) owns the means of production and distribution. The ACA doesn't take medicine out of the hands of health-care providers. It is, in fact, a boon for private insurance companies, who can expect to see enrollment skyrocket in states that expand Medicaid under the act. It does not specify limits on medical care patients can receive, nor does it specify treatment. The act expands access to health care and regulates some aspects of the industry; it doesn't take it over.

- False. An Independent Payment Advisory Board of health-care pros will study costs and propose ways to curb them. The board has no say in individual treatments, nor can it reduce benefits or increase premiums. Congress can overrule the board's decisions.

- False.

- False. The ACA doesn't change a law, in place since 1977, which states that no federal funds can be used for abortions except in cases of rape, incest or where the life of the mother is endangered. Under the ACA, state governments can restrict plans that cover abortions in their exchanges, and no private insurers can be forced to cover them. Before choosing a plan, consumers will be told whether a plan covers abortions; if they choose a plan that does cover them, a portion of the premium will be held separately to ensure no taxpayer funds are used to pay for a procedure.

- False. To the contrary, the increased numbers of people with access to health care will create demands for more doctors, nurses and a whole host of supporting players, from x-ray technicians to administrative assistants. Mississippi's University Research Center estimated that the state would see about 9,000 new jobs if it expands its Medicaid program under the Affordable Care Act. Gov. Phil Bryant is against expansion.

- False. The health-insurance industry has dominated medicine for decades, making fee-for-service the predominate model. That system has exploded the number of services--including tests, procedures and drugs--patients receive. Hospitals, doctors and other providers are paid for each one, giving them ample incentive to "go for the gold" instead of giving appropriate care to each patient. A 2009 Dartmouth Atlas of Health Care study estimated that patients pay about $700 billion annually on unnecessary treatments that don't make them healthier. This is the type of wasteful spending the Payment Advisory Board is designed to curb.

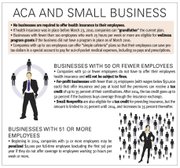

ACA and Small Business

• No businesses are required to offer health insurance to their employees.

• If health insurance was in place before March 23, 2010, companies can "grandfather" the current plan.

• Businesses with fewer than 100 employees who work 25 hours per week or more are eligible for wellness program grants if the business did not have a program in place as of March 2010.

• Companies with up to 100 employees can offer "simple cafeteria" plans so that their employees can save pre-tax dollars in a special account to pay for out-of-pocket medical expenses, including co-pays and prescriptions.

Businesses with 50 or Fewer Employees

• Companies with 50 or fewer employees do not have to offer their employees health insurance and will not be subject to fines.

• For-profit businesses with fewer than 25 employees (with wages below $50,000 each) that offer insurance and pay at least half the premiums can receive a tax credit of up to 35 percent of their contributions. After 2014, the tax credit goes up to 50 percent if the business buys coverage through the insurance exchange.

• Small Nonprofits are also eligible for a tax credit for providing insurance, but the amount is limited to 25 percent until 2014, and increases to 35 percent thereafter.

Businesses with 51 or More Employees

• Beginning in 2014, companies with 51 or more employees may be penalized $2,000 per full-time employee (excluding the first 30) per year if they do not offer coverage to employees working 30 hours per week or more.

More stories by this author

Support our reporting -- Follow the MFP.

Comments

Use the comment form below to begin a discussion about this content.

comments powered by Disqus